Pakistan’s Economic Reset: From Crisis to Confidence (2023–25)

A Crisis Narrative That Missed the Real Story In 2023, much of the global coverage of Pakistan painted a picture of collapse. A currency slide pushed inflation to a 48-year high, the policy rate...

A Crisis Narrative That Missed the Real Story

In 2023, much of the global coverage of Pakistan painted a picture of collapse. A currency slide pushed inflation to a 48-year high, the policy rate reached a record 22 percent, foreign reserves fell below four weeks of import cover, and default seemed imminent. Multinationals began restructuring or leaving, and commentators labelled the economy “uninvest able.” But those same shocks forced a disciplined reset rather than a free-fall. Between 2023 and 2025 Pakistan undertook painful reforms, cutting the current-account deficit, overhauling fiscal policy, and courting investors in technology, mining, and logistics. The result is a more resilient economy whose recovery now deserves fair recognition.

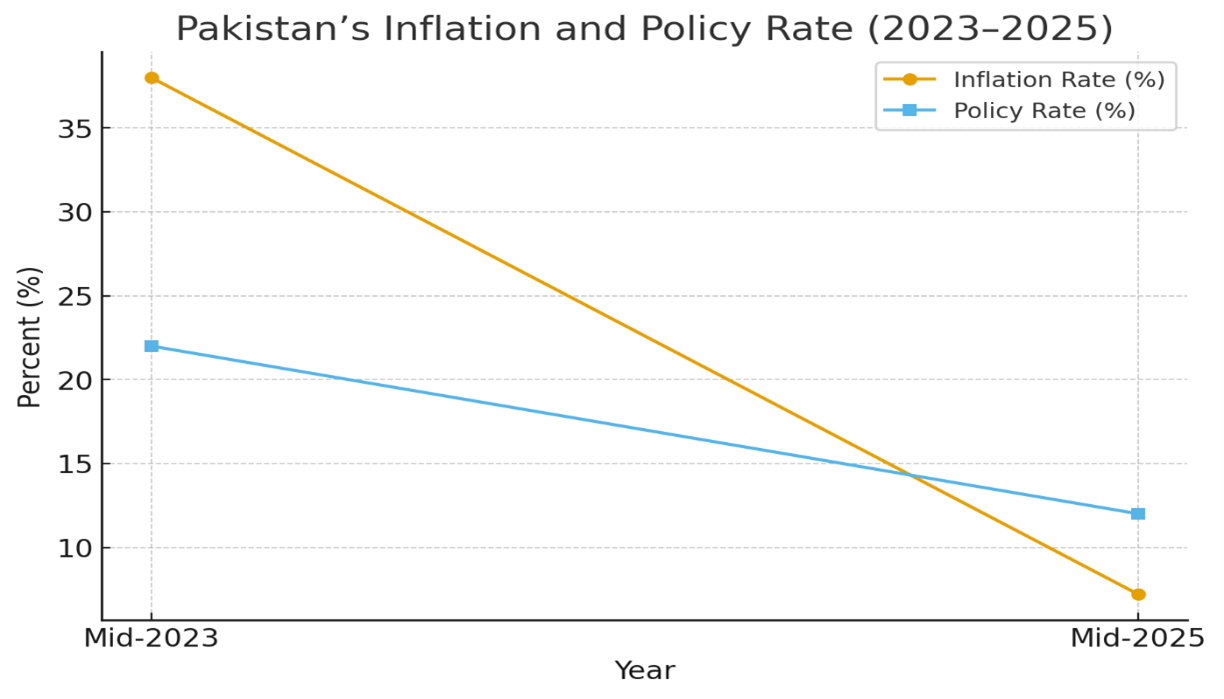

From Emergency to Disinflation

In mid-2023, inflation exceeded 38 percent and the central bank rose the policy rate to 22 percent to combat inflation. These emergency steps, combined with IMF-backed fiscal restraint, curbed domestic demand but prevented a balance-of-payments meltdown. By mid-2025, headline inflation had eased to 7.2 percent as food and fuel prices stabilized. With inflation in single digits and real rates positive, the State Bank cut its benchmark policy rate from 22 percent to 11 percent, which some analysts estimate saved the government about Rs 700 billion in interest costs. Disinflation reflected new discipline: flexible exchange rates, reduced subsidies, and controlled imports that prioritized essentials over consumption.

External Accounts: From Deficit to Surplus

Pakistan’s external position strengthened notably during FY 2025. After years of persistent deficits, the current account recorded a surplus of about US$ 1.2 billion (0.3 percent of GDP) in the first half of FY 2025, compared with a deficit of US$ 1.1 billion in the same period a year earlier. Foreign exchange reserves, which had declined to around US$ 4.4 billion in early 2023, rebounded to US$ 14.5 billion by June 2025, providing roughly 2.5 months of import cover, according to the State Bank of Pakistan. The rupee stabilized as the central bank met external debt obligations and cleared pending foreign-exchange backlogs, while improved external financing eased pressure on the balance of payments. Public debt remained elevated but showed modest consolidation, with debt-to-GDP ratio easing from about 75 percent of GDP in FY 2023 to roughly 73 percent in FY 2025, reflecting tighter fiscal policy and slower domestic borrowing. Although these gains mark a welcome stabilization, Pakistan’s medium-term outlook still depends on sustaining fiscal discipline, strengthening exports, and reducing reliance on short-term external inflows.

Fiscal Consolidation and Reform

Fiscal discipline anchored Pakistan’s recovery. The budget deficit narrowed sharply from 4.7 percent of GDP in the first half of FY 2024 to 2.8 percent in the same period of FY 2025, while the primary surplus nearly doubled to a record 6.6 percent of GDP, the strongest in decades. Sustained subsidy rationalization, new taxation measures on retail and real estate, and higher petroleum levies strengthened revenue credibility and improved fiscal space. Although overall investment temporarily eased to 13.1 percent of GDP in FY 2024, the government pivoted towards mobilizing private capital through dynamic public–private partnerships and investor-friendly reforms. The Special Investment Facilitation Council (SIFC), led by the Prime Minister with institutional backing from the military, expedited project approvals, enhanced coordination across agencies, and reinforced policy continuity, helping restore investor confidence and signaling Pakistan’s commitment to long-term stability and growth.

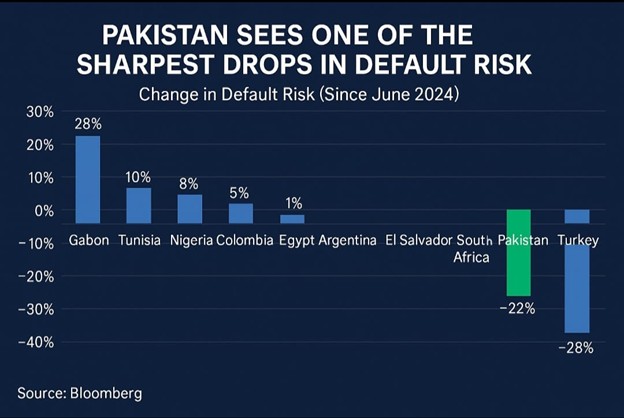

Sovereign Risk and Credit-Rating Rebound

Pakistan’s reputational turnaround is visible in sovereign-risk indicators. Credit default swap spreads fell sharply, reaching around 505 basis points by late 2024. In April 2025, Fitch upgraded Pakistan to B– (from CCC+) on the strength of improving fiscal and external metrics. In July 2025, S&P Global raised its sovereign rating to B– from CCC+, citing more stable finances and IMF support. In August 2025, Moody’s upgraded Pakistan from Caa2 to Caa1, pointing to an improved external position, rising reserves, and consistent debt servicing. These upgrades have helped reduce borrowing costs, revive access to syndicated credit, and reinforce the narrative that Pakistan is restoring sovereign creditworthiness.

Foreign Investment: Restructuring, Not Retreat

Several multinationals have adjusted their Pakistan exposure, but in many cases, the adjustment has meant ownership change rather than full exit. In June 2023, Shell Pakistan announced its intention to divest a 77.42 percent stake as part of a global portfolio review. In November 2024, Saudi-based Wafi Energy (affiliate of Asyad Group) completed the acquisition and now holds about 87.78 percent of the company, while retaining the Shell brand via a licensing arrangement in Pakistan. In 2024, Pfizer Pakistan sold its Karachi manufacturing plant and associated product assets to Lucky Core Industries. In the telecommunications sector, Telenor Pakistan is being acquired by PTCL (merging with Ufone); the Competition Commission of Pakistan approved the transaction with conditions to protect competition. More recently, P&G announced in October 2025 that it will wind down its manufacturing and commercial operations in Pakistan, including Gillette Pakistan, and shift to a third-party distributor model to continue servicing the market.

Meanwhile, capital inflows are rising and contradict narratives of widespread capital flight. From July 2024 to February 2025, net FDI in Pakistan reached US$ 1.618 billion, up about 41 percent year-on-year, with the power sector alone attracting around US$ 578 million. The IT industry continues to perform strongly: from July to March FY2025, IT exports hit US$ 2.825 billion, generating a trade surplus, and freelancers contributed roughly US$ 400 million in remittances. These data suggest that international capital is reorienting toward energy, infrastructure, and the digital economy, and that while some multinational structures are being reshaped, the availability of operations and products largely endures under new ownership.

A Pivot Toward Gulf and Asian Partners

From 2024 onward, Pakistan strengthened its engagement with regional investors. In May 2024, Prime Minister Shehbaz Sharif secured a US$ 10 billion investment pledge from the UAE across sectors such as energy, logistics, ports, and technology. Around the same time, Pakistan and Saudi Arabia reaffirmed their intent to expedite a US$ 5 billion investment package, including in minerals and related projects. Pakistan and Malaysia have taken a major step toward deepening economic and diplomatic ties with the signing of six accords during Prime Minister Shehbaz Sharif’s recent visit to Kuala Lumpur. Among the key outcomes was a landmark $200 million Halal meat export deal, marking Pakistan’s largest such order to Malaysia. The agreement not only strengthens Pakistan’s position as a credible Halal-certified exporter but also opens access to Malaysia’s $3 billion Halal food market and broader ASEAN trade opportunities.

Meanwhile, Pakistan’s outward investment in Malaysia has reached approximately US$ 397 million by early 2025, reflecting the growing depth of cross-border enterprise and investor confidence between the two nations. While not all deal sizes or execution timelines have been publicly confirmed, these developments underscore Pakistan’s emerging role as a bridge for Gulf and Asian capital entering South Asia, particularly in infrastructure, energy, and the digital economy.

Both nations also finalized memorandums of understanding covering education, Halal certification, tourism, SMEs, and anti-corruption cooperation, reflecting a shared commitment to sustainable growth and innovation. Prime Minister Shehbaz Sharif hailed the deals as a “welcome step” that will create jobs, boost Pakistan’s livestock sector, and pave the way for future trade in other Halal products like food, cosmetics, and pharmaceuticals.

Exporting Innovation Instead of Importing Crises

Pakistan’s growth model is shifting from consumption to production. The IT sector, already one of the world’s largest freelance talent pools, grew rapidly as firms were allowed to retain 50 percent of export earnings in foreign currency. The government launched a national minerals company to attract exploration bids for copper and rare earths, while bumper wheat and rice harvests restored food security and lifted exports. Together with SIFC-backed projects in renewables, logistics, and defence production, these measures are transforming Pakistan into a more self-reliant, export-oriented economy.

Why The Narrative Must Change

Pakistan’s challenges, narrow taxation, poverty, and political volatility, remain serious managed to reduce its inflation. Yet, they don’t define the full picture. Between mid-2023 and 2025, Pakistan cut interest rates by 1,100 basis points (11 percentage points), from a peak of 22% in June 2024 to 11%, reflecting confidence in declining inflation and improving stability. Investors like the UAE and Saudi Arabia don’t commit billions of dollars unless they trust a country’s direction. In Pakistan’s case, that trust stems from a sequence of difficult but essential reforms: tightening monetary policy to curb inflation, removing costly energy subsidies, broadening the tax base, market determined exchange rate, and restructuring loss-making state enterprises.

During the crisis years, the government allowed the rupee to find its real market value, phased out unsustainable fuel and power subsidies, and created the Special Investment Facilitation Council (SIFC), bringing civilian and military institutions together to fast-track approvals and ensure policy continuity. These steps, paired with efforts to expand the tax net and streamline governance, signaled that Pakistan was serious about long-delayed structural reform. Those measures restored macroeconomic credibility. The breathing space gained through higher reserves, lower inflation, and positive real interest rates must now be used to deepen reforms, widening the tax base, modernizing state enterprises, and strengthening the rule of law. A more disciplined and confident Pakistan is emerging, one that has learned from crisis rather than succumbed to it. For investors willing to look past outdated headlines, the country offers not a collapse to avoid, but a comeback worth watching.